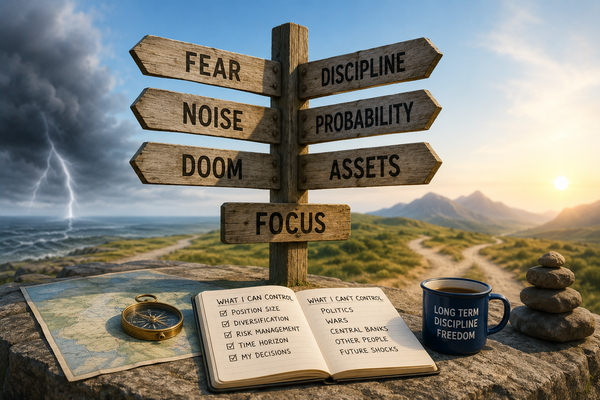

If there was a single undercurrent running through the most recent monthly Q&A call, it was fear.

Fear of AI destroying livelihoods and concentrating power.

Fear of custody risk and the “Great Taking.”

Fear of governments seizing commodity assets through windfall taxes and nationalisation.

Fear of a closed Strait of Malacca, the war in the Middle East intensifying, a deflationary collapse that wipes out hard asset theses.

Fear that Fannie Mae accepting crypto collateral is the next step toward digital serfdom.

Fear that the elites have already won.

We understand where it comes from. All media is built to manufacture this stuff, and we have a lot more access to it than ever. Podcasts these days are either corporate-manufactured jibber jabber dressed up as “content,” or some new trending YouTube/X personality with a microphone and a thesis about the end of civilisation.

None of them are managing money — and that’s the key point. Commentators who don’t have to put capital on the line can afford to be as alarmist as the algorithm rewards them for being.

They get to raise a concern and then stop. They never have to answer the second question: given all that, what are you actually doing with your portfolio?

Our answer doesn’t change much. You manage risk through probability, position sizing, and diversification. You don’t eliminate it, because you can’t. The world doesn’t — nor has it ever — work like that. If a risk is already priced in, the security is a buy. If it isn’t, you move on, or you buy a smaller size. Australian coal miners got hit with a windfall tax and we still own them because the valuation still made sense.

Russian equities taught us the same lesson from the other direction — we were right about the companies and wrong about the West sanctioning the securities. Position sizing is the reason we still came out ahead despite 10% of our portfolio being marked down to zero.

The discipline is what works across scenarios. The narrative is what varies.

Our portfolio is already positioned for the things members are worried about. We hold hard assets because every debt cycle in 500 years of history has ended the same way: default, or default by inflation, with capital flowing back into hard assets.

We hold energy because you cannot run an AI-driven economy, a re-industrialising West, or a growing emerging-market consumer base without it. We hold emerging markets because the post-2008 outperformance of US equities was the anomaly, not the baseline. None of that requires a specific doomsday scenario to pay off. It just requires the slow grind of history to keep rhyming with itself.

If one thing is worth carrying forward, it is this: worry about what you can control, tune out commentators who cannot tell you what they are doing with their own capital, and focus on asymmetry.

That is where returns come from. It is also — not coincidentally — where peace of mind comes from.

Editor’s Note: The forces driving today’s fear-filled headlines are part of a much bigger shift now unfolding across the economic, political, and cultural landscape. Our free special report shows what may lie ahead, what it could mean for your money and personal freedom, and how to think about staying one step ahead. Get your free copy.