Everyone remains positioned for one big theme: deflation.

Where to invest? An article from Bloomberg has the answer. Goodness knows how they select the “experts”:

So what do the geniuses suggest?

- Private credit

- Investing in supply chains (however you achieve that)

- Bet on Bitcoin

- Cybersecurity

- Global 60/40

Then there is this:

Investing in fixed income (aka bonds) at the end of a debt supercycle is like eating vindaloo that has been left out on the bench for a week and has gone furry.

Notice also that despite the commodity markets already having turned, there is nothing here suggesting investing in energy, let alone oil and gas producers, coal miners, associated service companies, agricultural companies, fertilizer, gold, Greek or Argentinian equities, shipping… and the list continues.

We doubt that allocations to hedge funds will lead to any over exposure to energy.

From the article:

Portfolio investors have become exceptionally bearish about crude oil as global economic growth slows and production cuts from Saudi Arabia and its OPEC⁺ allies have failed to lift prices.

Hedge funds and other money managers sold the equivalent of 64 million barrels in the six most important petroleum-related futures and options contracts in the seven days ending June 27.

The net position across the three major crude contracts fell to 205 million barrels, the lowest since at least 2013, when data became available in this form.

Bullish long positions exceeded bearish short ones by a ratio of just 1.86:1 (2nd percentile for all weeks since 2013).

The last time fund managers were so pessimistic about crude prices was during the first wave of the coronavirus pandemic in 2020 and before that during the volume war between oil producers in 2014/2015.

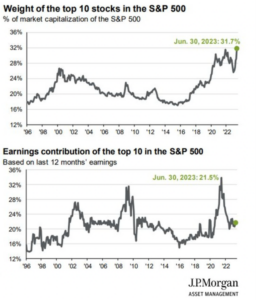

The pessimism towards crude prices is reflected in the makeup of the S&P 500 and the performance of value vs growth. Buying the S&P 500 or index hugging mutual funds has never been this concentrated.

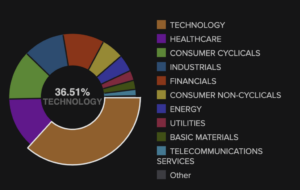

So tech makes up some 36% of the S&P 500, even though a few big hitters like Amazon and Meta aren’t classified as tech.

So three companies make up near 20% of the S&P 500. We cringe at having more than a 2% weighting to any one stock or 10% to any one sector as being too risky. The S&P 500 (by default the vast majority of investors) makes us look like boring old ultra conservative farts. Perhaps we aren’t taking enough risk?

This brings us back to value vs growth: value relative to growth is still more unloved than it was during the height of the TMT bubble.

The more one looks at what the “experts” suggest buying, what family offices are supposedly buying, and how out of favour value is relative to growth, the more one comes to the conclusion that the vast majority are positioned for a deflationary theme.

This implies that inflation has peaked and will continue to move down over the coming months, if not years, which implies that the cost of energy will not rise and interest rates have peaked — it is all the same broad theme.

We feel very comfortable taking the other side of how the crowd is positioned. The “inflation” theme is light years (10 years or more) from being a crowded trade.

Editor’s Note: The Western system is undergoing substantial changes, and the signs of moral decay, corruption, and increasing debt are impossible to ignore. With the Great Reset in motion, the United Nations, World Economic Forum, IMF, WHO, World Bank, and Davos man are all promoting a unified agenda that will affect us all.

To get ahead of the chaos, download our free PDF report “Clash of the Systems: Thoughts on Investing at a Unique Point in Time” by clicking here.