“It was the single most important financial event of my career.”

That’s how my friend and resource-investing legend Rick Rule once described his experience in the uranium market—a market defined by extreme imbalances between supply and demand, producing colossal boom-and-bust cycles.

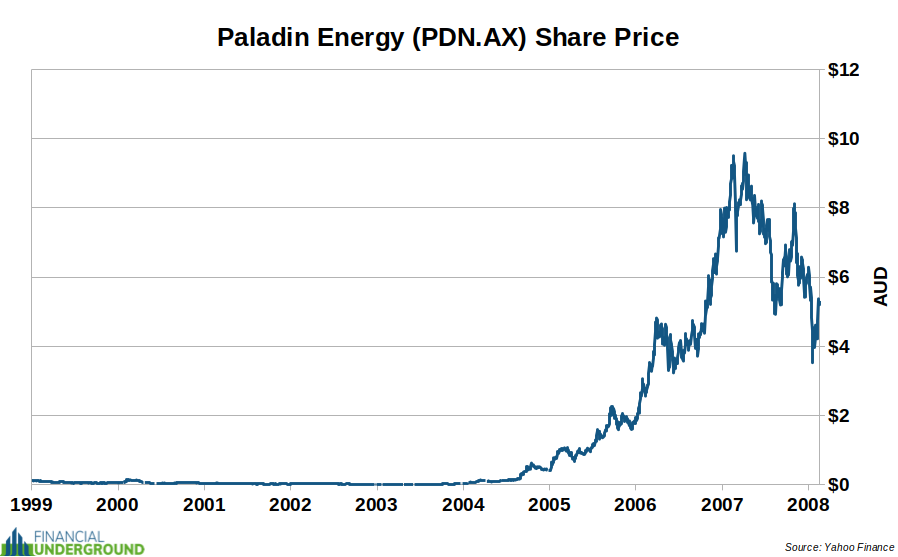

Rick was referring to Paladin Energy, a uranium stock that exploded during the last uranium bull market, rising from less than one cent (AUD $0.007) at its April 2003 low to AUD $9.57 at its peak in April 2007.

That represents a gain of more than 130,000%—a greater than 1,000-fold increase.

In theory, a $1,000 investment could have turned into more than $1 million with perfect timing.

That, of course, is unrealistic. But even investors who were early—or late—by a year still had the opportunity to generate extraordinary returns.

Paladin was an outlier and the best-performing uranium stock of that market cycle. Other uranium companies also saw dramatic gains, though none matched Paladin. And as always, it’s critical to remember that past performance is no guarantee of future results.

Still, the lesson is unmistakable.

Uranium bull markets, when they arrive, tend to be violent, selective, and exceptionally rewarding for those positioned correctly.

For investors, that combination—rising strategic importance, constrained supply, accelerating demand, and a history of explosive cycles—is powerful. But not all exposure is created equal. The uranium market is small, complex, opaque, and carries serious risks.

To understand where the real opportunities—and pitfalls—lie, we need to look closely at the global uranium industry.

Uranium Industry

Nuclear power plants account for most uranium demand, which is inseparably linked to the uranium price and market cycles.

A nuclear power plant produces energy by splitting uranium atoms. The energy released boils water, creating steam that drives turbine generators. These plants use fuel made from uranium ore. First, miners extract the ore from the ground. Then it is enriched and fabricated into fuel pellets.

According to the American Nuclear Society, one nuclear fuel pellet—about the size of a small gummy bear—has as much energy density as three barrels of oil, 2,000 pounds of coal, or 17,000 cubic feet of natural gas.

According to the World Nuclear Association, 33 countries use nuclear power, with around 438 operable reactors worldwide. Seventy reactors are currently under construction, and another 111 are planned.

Each year, the world’s active nuclear power plants require approximately 174 million pounds of U₃O₈, commonly known as “yellowcake” to operate. This demand is inflexible, meaning power plants must secure that uranium or the lights go out.

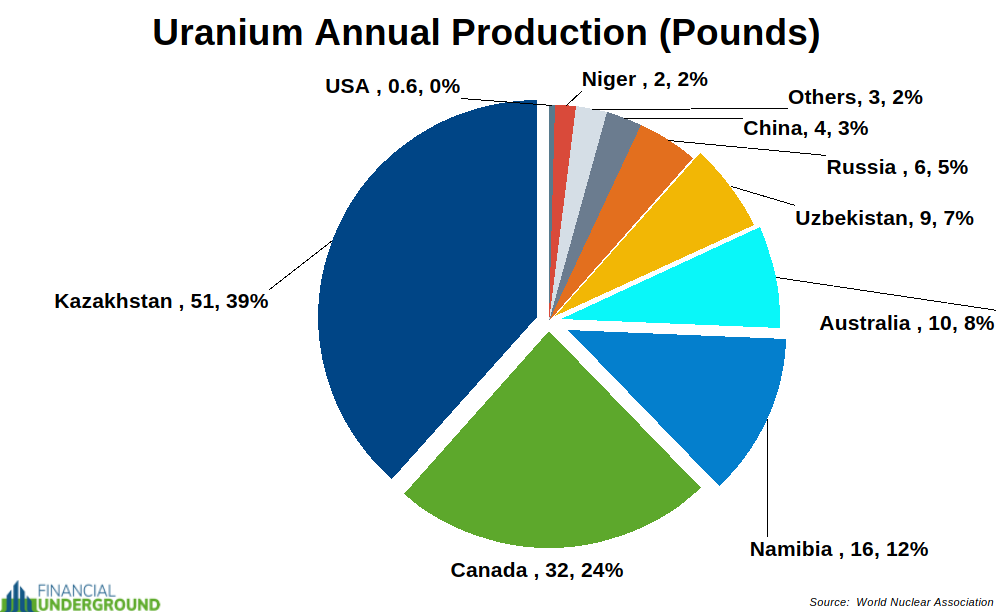

This inflexible demand is paired with a precarious supply situation, where most uranium production occurs in geopolitically unstable regions such as Africa and Central Asia.

Further, it often takes 7–10+ years to bring a new mine online, and in many cases longer, depending on jurisdiction and project complexity. As for existing mines, once producers take mines offline—often because the uranium price has fallen below the cost of production—it can be difficult to bring them back quickly. Uranium mines don’t have easy on/off switches.

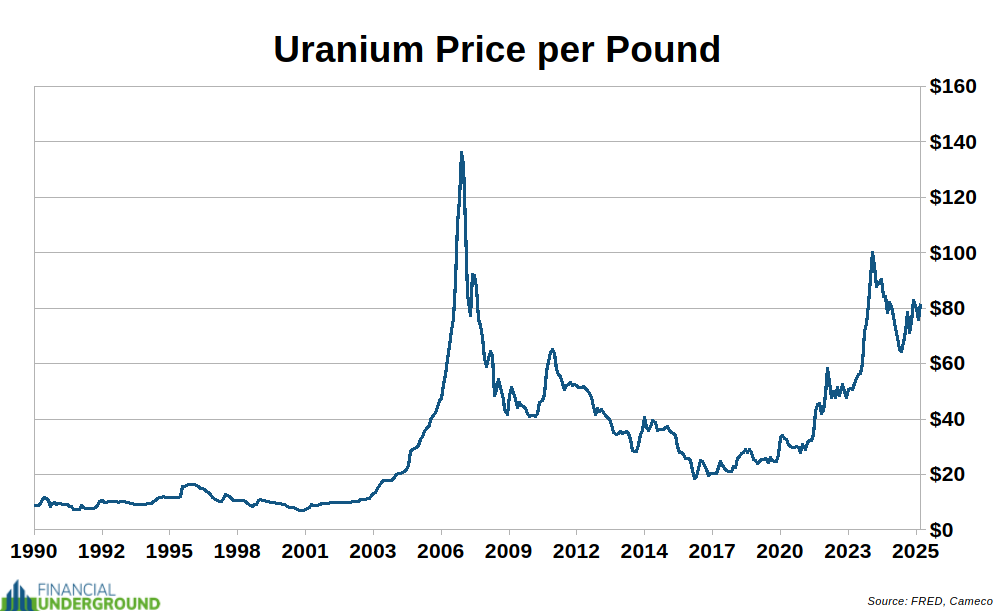

Earlier industry forecasts understated true costs by focusing on cash costs rather than full sustaining costs. What was once thought to require $70–75 uranium prices to incentivize supply is increasingly viewed as outdated. Given inflation, delays, and rising capital costs, many analysts and market participants now talk about incentive levels in the high-$80s to $100+ per pound range.

In short, it is difficult for producers to ramp up production during rising uranium demand. It often takes years for them to catch up. As a result, the only way for the market to resolve itself is through the price. That’s why the uranium price can have extraordinary spikes.

However, the uranium market often doesn’t just settle into equilibrium during these periods. The uranium price often overshoots where it needs to go to balance the market, creating an enormous bull market that turns into a massive bear market. This cycle has played out before, and I think it will occur again.

While the price of uranium and uranium stocks have started to take off recently, I don’t think we are anywhere near the top for this cycle.

Demand for uranium is set to increase drastically.

Currently, there are about 438 operable nuclear reactors worldwide. Another 70 reactors are under construction, and another 111 are planned.

China accounts for the lion’s share of future demand. The World Nuclear Association lists 37 reactors under construction, 44 planned, and 145 proposed in China. Beijing has also stated ambitions that are frequently summarized as building about 150 new reactors between 2020 and 2035.

China is expected to overtake the US as the world’s largest uranium consumer by 2030.

China needs nuclear power to support its growing economy and reduce its huge air pollution problem. Today, coal is still China’s primary power source, but it carries a high cost. Air pollution in Chinese cities is a serious health risk.

This is a big reason why the Chinese government aggressively pursues nuclear energy. In short, China has the most ambitious program for constructing new nuclear reactors globally.

The Chinese government rules by consensus, and they’re careful long-term planners. So when they make a strategic decision to include nuclear energy as a crucial part of their energy security, I have no doubt they are committed to seeing it through. They have the political will to pull it off and the financial, technological, and physical resources to do it.

Mines produce around 157 million pounds of uranium each year, while the world consumes about 174 million pounds. Global inventories supply the difference—roughly 17 million pounds.

Primary supply-demand modeling from analysts shows persistent deficits. Near-term deficits are often modeled in the 10–15 million pounds of uranium per year range, with some models rising meaningfully later in the decade depending on reactor buildout, mine depletion curves, and project execution timelines.

Getting accurate figures on global uranium inventories is challenging because governments and companies keep that information confidential. However, they will not allow inventories to become too low for energy security reasons.

Analysts estimate worldwide uranium inventories to be around 2-3 years’ worth of coverage. However, it is essential to stress that this is just an estimate—nobody knows how much uranium is in global inventories.

We know utilities generally prioritize security of supply through multi-year coverage via a mix of physical inventories and long-term contracts. If inventories tighten in a supply-constrained environment, we could soon see power companies (and governments) scramble to secure their supplies in a tight supply environment.

Historically, uranium bull markets haven’t been driven by a single event, but by a series of small supply disruptions combined with steadily falling inventories. That same dynamic is playing out again, with utility contracting rates now rising sharply after a decade of under-replacement, setting the stage for continued tightening in the msarket.

Once utilities realize the deficit isn’t temporary but could last decades, the rational response will be to lock in very long-term contracts—10 to 20 years—at whatever price is available. That kind of panic contracting has happened before. When one respected buyer signs an unusually long and expensive contract, others will panic and rush in. At that point, producers won’t have enough supply to offer long-dated contracts at any price, pushing prices sharply higher.

Ultimately it is likely utilities will only act once prices force them to. When they finally do, it’s likely they will rush into the market aggressively, competing with each other for limited supply and driving uranium prices sharply higher in a very short period of time.

Uranium is a perfect case study in the world we’re entering: inflexible demand, fragile supply, and prices that don’t “adjust” so much as they spike once everyone scrambles for security at the same time.

And that dynamic isn’t limited to uranium. It’s starting to show up across energy, critical minerals, and strategic supply chains as governments treat essential inputs like national-security assets—and as shortages get solved the same way they always do: through higher prices and sudden volatility.

If you want the bigger framework behind these kinds of moves, I wrote a free PDF report: The Most Dangerous Economic Crisis in 100 Years… the Top 3 Strategies You Need Right Now.

It connects the economic, political, and cultural forces driving today’s tightening world, explains the risks they create for your wealth and freedom, and lays out three concrete strategies you can use immediately to protect yourself—and position for what comes next.